Despite ongoing quarantines, shelter-in-place orders, and other stringent measures, COVID-19 has continued to spread. As deaths climb and the human toll mounts, leaders are focused on containing the virus and saving lives. In parallel, efforts are under way to mitigate the devastating economic consequences of COVID-19, which include business shutdowns, record unemployment, and unprecedented drops in gross domestic product (GDP) across many countries.

The semiconductor industry, which has historically been a major source of high-tech jobs, is among the many sectors that have had to adjust their production planning and operations as COVID-19 shifts demand for major semiconductor end applications. In addition to exploring the impact of such changes on semiconductor demand, this article provides insights about the industry’s evolution post-crisis and outlines how semiconductor leaders should prepare themselves for the next normal.

Impact of COVID-19 on global semiconductor demand

The COVID-19 crisis is unprecedented in our time. While the recession during the financial crisis from 2007 to 2008 was driven by stagnating consumer demand, the COVID-19 situation induced a shock to both global demand and supply, creating a dual challenge. This unique phenomenon makes it difficult to extrapolate from past crises to make predictions.

Nevertheless, this article aims to provide guidance on how semiconductor demand will shift in the short- and mid-term—taking into account extensive surveys, research on the recovering Chinese market, and global GDP projections. Our GDP projections in this article are based on two of the nine scenarios that McKinsey developed for global GDP recovery, both of which assume that the spread of coronavirus is eventually controlled and catastrophic economic damage is avoided. In the first scenario, global GDP recovers in the fourth quarter of 2020; in the second, recovery is delayed until late 2022.1 All demand forecasts are shown as a percentage of 2019 market sizes.

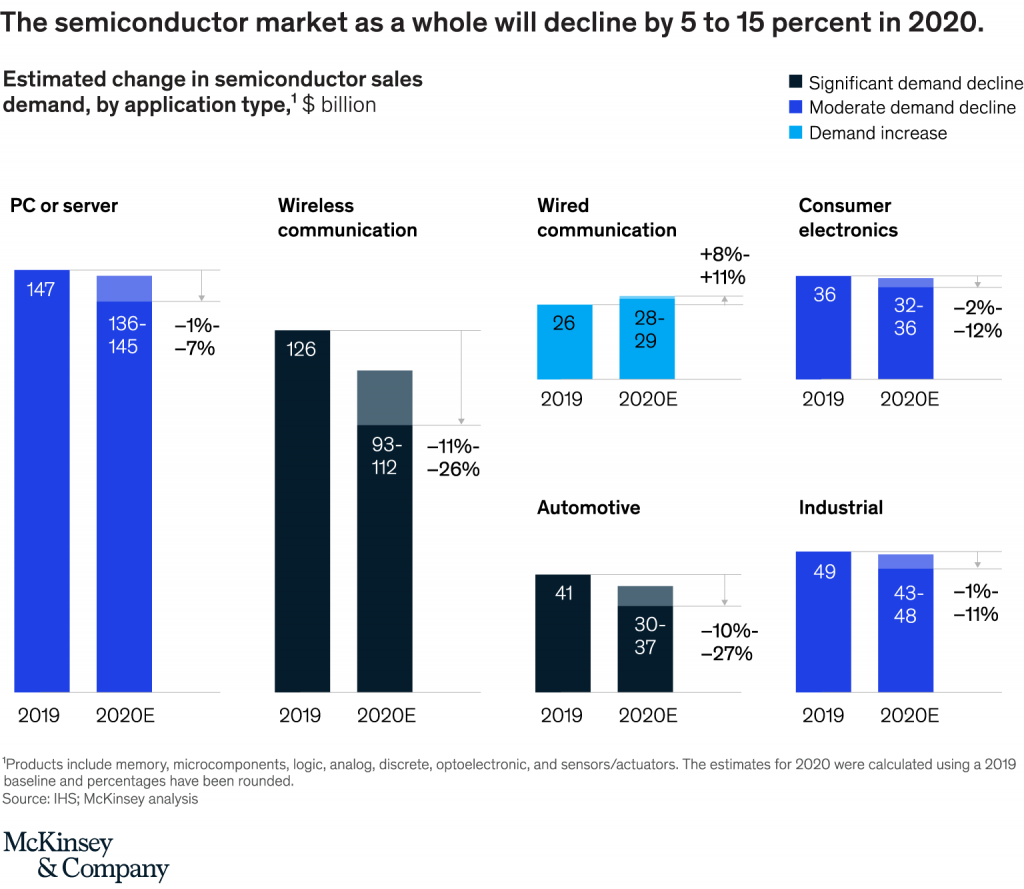

Based on the two scenarios we evaluated, we expect demand to decline by 5 to 15 percent for the semiconductor industry as a whole this year compared to 2019 (Exhibit 1).

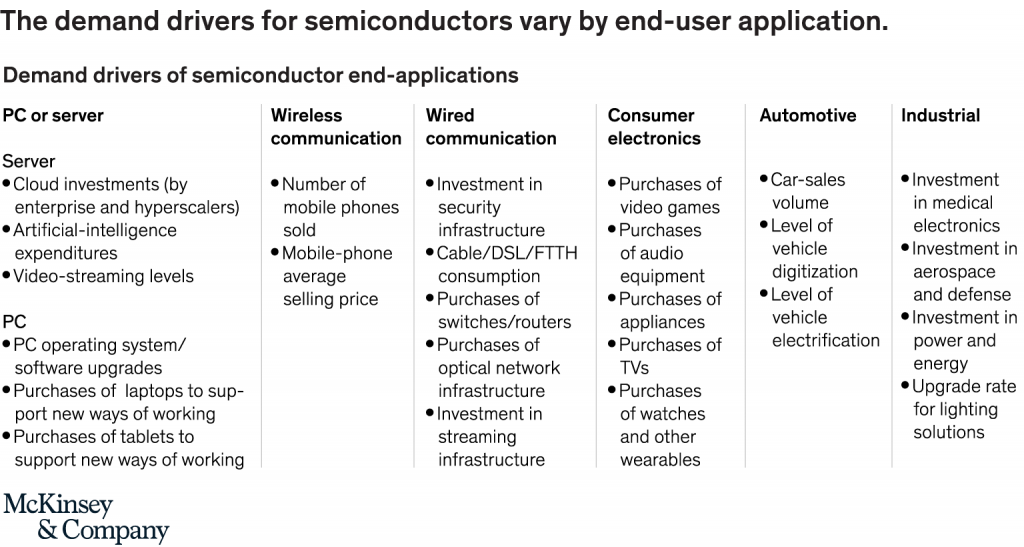

Breaking down this projection by major end markets—PC or server, wireless communication, wired communication, consumer electronics, automotive, and industrial applications—shows that demand shifts vary greatly, with steep declines anticipated for some markets and gains expected in others. These differences can be explained by the diversity of underlying trends that affect demand for semiconductors, and the varying impact of macroeconomic forces on each end market. (See sidebar, “Demand drivers of semiconductor end-applications.”)

PC or server

We expect chip demand for the PC and server end market to drop by 1 to 7 percent this year, with results varying by product.

Demand for PC semiconductors will decline by an estimated 3 to 9 percent in 2020, mostly because companies will delay planned hardware upgrades and other long-term migration projects. Stable laptop and tablet demand will partly offset this drop, since many consumers will upgrade their private IT infrastructure to support their work or homeschooling activities, even if they are cutting back in other areas. These one-time IT equipment upgrades will not be repeated to the same extent in later years if the downturn persists and consumers cut back spending even further. This fact, combined with enterprises decreasing computer replacements to manage their liquidity, could further erode semiconductor sales after 2020 if the crisis persists.

Through late 2020, the semiconductor market for servers could increase by 1 to 7 percent, driven by a strong uptick in video streaming and conferencing as more people work from home. Demand for enterprise IT and enterprise cloud solutions is expected to remain stable or show a minor decline as some companies cut IT budgets while others accelerate their cloud-migration plans. Increased server demand may not persist past 2020, however. If the global economy continues to struggle after the fourth quarter of 2020, more companies will cut IT budgets—a trend that will outweigh any additional increases in video streaming.

Wireless communication

Demand for semiconductors used in wireless communication applications will see one of the sharpest drops in 2020, with an expected decrease of 11 to 26 percent. The level of mobile-phone sales, the primary demand driver in this category, has historically been well correlated with GDP and thus is expected to drop significantly over the coming months. (Sharp decreases have already been documented in areas where COVID-19 is prevalent, especially China). We also expect consumer preferences to shift to less expensive phones, which will also negatively affect demand for semiconductors. The recovery of mobile-phone sales will vary by geography, with China likely to see an uptick before Europe and the United States, since its economy is closer to recovery.

For wireless communication infrastructure—5G in particular—we expect to see two different demand patterns. In areas that have not launched 5G networks, telecom providers will likely postpone investments and instead focus on improving their existing networks to accommodate rising data traffic. By contrast, some telecom providers in areas that already have 5G will double down on their investments, especially if governments provide subsidies in an attempt to stimulate the local GDP.

Wired communication

Demand for semiconductors used in wired communication applications will increase by 8 to 11 percent in 2020 because of several pandemic-related factors, including:

- more security upgrades for existing enterprise infrastructures as more employees work from home

- a more than 50 percent increase in fixed broadband usage in some countries, leading to more purchases of cable/DSL and wireless routers as workers upgrade internet connections in private home offices

- higher internet traffic, which will spur demand for switches and routers

- greater demand for cloud services and associated computing nodes, which will increase the need for optoelectronics in data center fiber connections

- a more than 40 percent increase in video streaming across many networks

Even if the economic downturn persists after 2020, demand for semiconductors used in wired communication will still grow. Annual growth may not remain as high as the 8 to 11 percent seen in 2020, however, since many of the mentioned investments are one-time purchases that will reduce future replacement needs.

Consumer electronics

Semiconductor companies provide components for many consumer-electronics products, including video games, televisions, and watches. Consumers use discretionary funds to purchase most products in this category, so demand is highly correlated with local GDP. We expect demand for consumer-electronics semiconductors to drop by 2 to 12 percent in 2020. While significant, this decrease is lower than the drop seen within wireless communication—another area where end-market sales are closely tied to local GDP.

Consumer electronics are faring better than wireless communication because of a recent rise in demand for gaming devices, audio equipment, and some kitchen appliances—a trend likely occurring because people are spending more time at home. Although this increase has partly offset the significant declines reported for other consumer-electronics products, it likely stems from one-off purchases and thus will not persist over time. In consequence, the decreased demand for consumer-electronic semiconductors will extend beyond 2020.

Would you like to learn more about our Semiconductors Practice?

Automotive

Sales of semiconductors for automotive applications primarily depend on car sales volume and the level of vehicle digitization and electrification. Since global automotive demand has already fallen sharply this year and will likely decline further over coming months, the automotive semiconductor market is expected to decrease by 10 to 27 percent in 2020. Semiconductor companies will likely not feel any effect until late in the second quarter, however, due to the long lead times of automotive semiconductors.

In terms of semiconductor demand, hybrid electric vehicles (HEV) and electric vehicles (EV) are particularly important, since they contain more semiconductors than combustion-engine vehicles. Currently, we expect that the decline in demand for HEVs and EVs will be similar to that for other vehicles, leaving their market share constant. That said, semiconductor companies should watch out for certain developments that might increase or decrease the share of HEVs and EVs in the market. For instance, increased government subsidies may spur additional demand for HEVs and EVs, while less stringent emissions regulations or continued low oil prices might push sales down.

Industrial applications

Within industrial applications, the major demand drivers for semiconductors include investments in medical electronics, aerospace equipment, power and energy products, as well as upgrades to lighting solutions. Demand is expected to decline for all of these end markets through 2020 as companies postpone infrastructure investments, reduce manufacturing activities, or decrease operations. Overall, semiconductor demand for industrial applications is expected to fall 1 to 11 percent this year.

For medical electronics, demand in certain medical-device categories that are directly related to the management of COVID-19, including ventilators, X-ray machines, and diagnostic tools, has sharply increased since the start of the outbreak. However, there will be even steeper demand declines in other areas that will offset such extreme demand spikes for critical treatment products because many hospitals are postponing purchases to improve liquidity.

Strategies for semiconductor companies

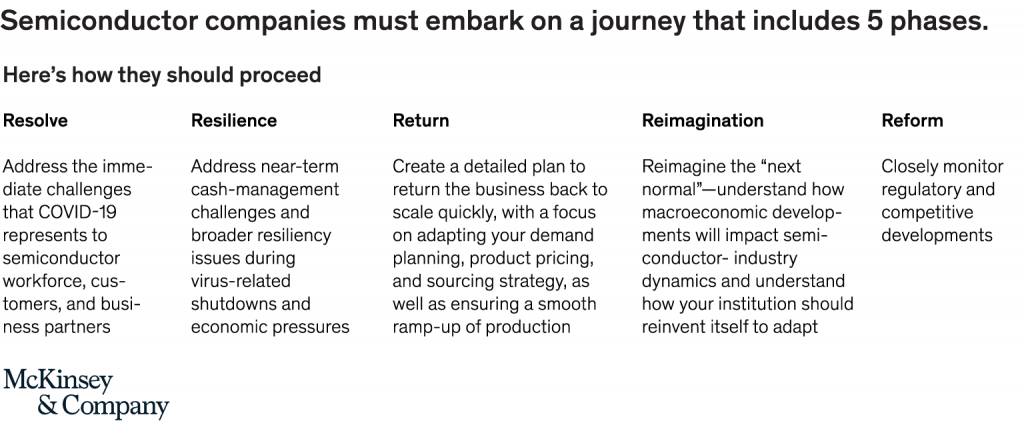

Like all business leaders, semiconductor executives are wondering how they can adapt to sudden changes in demand, as well as other uncertainties associated with COVID-19. They may find a path forward by following a framework that McKinsey created to assist companies on their journey to the next normal. It includes five stages: resolve, resilience, return, reimagine, and reform (Exhibit 2).

Most semiconductor companies have already passed through the first two phases or are currently addressing challenges related to reduced workforce availability and near-term cash management. Experience has also shown, however, that companies should do far more than handling operational challenges during economic downturns if they want to emerge stronger post-crisis. Despite focusing on operational issues that require immediate attention, semiconductor leaders would also benefit by thinking ahead—and that will involve progressing through the return, reimagine, and reform phases as quickly as possible.

Return

When planning for the return to the next normal, semiconductor leaders should determine if they need to revise any critical business activities in response to the changed demand dynamics. As they set their course, they may benefit by focusing on the following tasks:

- Adjusting demand planning. How long will it take until an increase or decrease in customer demand affects orders for semiconductors and how steep will the decline be?

- Revising production planning. Can the business adjust its production plans and make costs more variable to reflect changing customer demand and/or labor shortages?

- Revisiting sourcing strategy. How does the closure of country borders and the potential financial distress of suppliers affect sourcing operations?

- Revising product pricing. Will the company’s product-pricing strategy be affected by changing logistics costs and/or our customers’ willingness to pay?

- Revising previous business practices. Based on the company’s experience with remote work during the pandemic, do any business practices need to be revised, or even removed?

Reimagine

As semiconductor companies start to reimagine a new normal for their industry, they should create dedicated working teams that follow up closely on the following topics.

Changing industry dynamics. New technologies that helped in the fight against COVID-19 could permanently change how companies work. Some shifts in work processes and consumer behavior that arose during the pandemic might also persist, and these could open both new markets and routes to market. Semiconductor players might place more emphasis on digital marketing, for instance.

Growth stimulation. Governments may soon provide subsidies, such as incentives for further 5G roll outs, to stimulate the economy in multiple industries. Other government subsidies might encourage local production or investments in healthcare. Such changes could lead to faster technology adoption, and semiconductor companies might need to re-evaluate their product road maps.

Sourcing shifts. Companies along the value chain are likely to revise their sourcing strategies. For semiconductor players, this might involve further leveraging foundries and decreasing their reliance on critical suppliers.

Some shifts in work processes and consumer behavior that arose during the pandemic might also persist, and these could open both new markets and routes to market.

Reform

Throughout the reform phase, semiconductor companies should monitor changes in the following areas.

Regulatory environment. Trade tensions are unlikely to increase significantly over the short term, since economies are still highly interlinked and governments will likely be cautious about causing additional stress in industries that are still striving to recover. If governments decide to subsidize local sourcing and manufacturing activities, however, opportunities could open for fast movers.

Competitive environment. As the crisis drains liquidity from companies, and valuations take a significant hit (with high variance, depending on semiconductor end market exposure), we are likely to observe increased M&A activities. The companies involved should monitor potential regulatory constraints on foreign purchases.

Strategic next steps

As companies proceed through the five phases that will take them to the next normal, they could strengthen their muscles by evaluating and capturing strategic opportunities at a fast pace.

After the financial crisis of 2007 to 2008, the semiconductor companies that emerged strongest were those that implemented bold moves and thus contributed to reforming the industry. They maintained relatively higher capital expenditures and R&D spending compared with their competitors and were more active in pursuing M&As. Current leaders might want to consider similar options.

Before making such moves, semiconductor companies might want to reassess their baseline position, since the coronavirus pandemic may have altered it considerably, and then look at both potential opportunities and business threats that may arise over multiple time horizons. Companies must quickly move from strategic plans to action, however, since many opportunities may open up quickly and only be available for a limited time. Some leaders might want to define specific trigger points—events that will move them to act—as they create their plans.

Market dynamics in the semiconductor industry are rapidly changing. Demand is moving in different directions, and to different extents, depending on the application segment involved. As semiconductor players adapt to these changes and journey toward the next normal via bold and timely moves, they can help their businesses thrive.

About the author(s)

Harald Bauer is a senior partner in McKinsey’s Frankfurt office, Ondrej Burkacky is a partner in the Munich office, Peter Kenevan is a senior partner in the Tokyo office, Abhijit Mahindroo is a partner in the Southern California office, and Mark Patel is a senior partner in the San Francisco office.