Executive Interview with Ravi Subramanian, SVP & GM of the IC Verification Solutions, Siemens EDA

In this interview with Ravi Subramanian, he identifies the latest semiconductor trends, as well as what’s driving those trends, how they are affecting chip design and functional verification and why he is bullish on hardware-assisted verification.

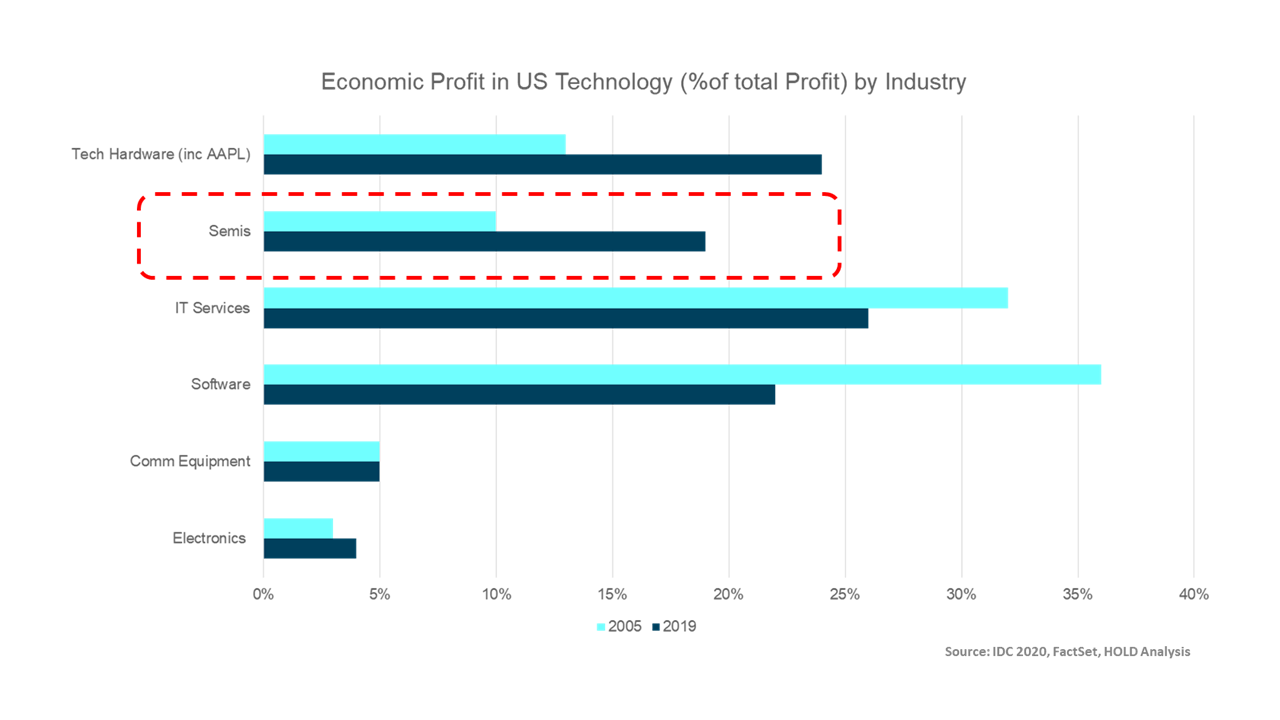

I want to start with a not necessarily well-known fact. A report from IDC published last year pointed to significant changes in semiconductor industry profits. Over the past few years, profits have been migrating from software to silicon and technology hardware.

The chart underscores the phenomena that over the last decade, industry profits in the U.S. economy moved to semiconductors and technology hardware. Source: IDC

The IDC graph shows a significant change in how profits have moved dramatically towards technology hardware and semiconductors over the past decade while electronics industry increasing contribution to worldwide GDP as we enter the era of digitalization.

Despite COVID, the growth we have seen in specific semiconductor markets is a dramatic difference compared to the semiconductor industry performance during prior downturns in 2000 and 2007.

As long as we have a rather loose monetary policy around the world, we should expect to see three things in 2021.

First, we should expect to see significant growth in semiconductors developed by companies that are not traditionally semiconductor companies as reflected in the rapidly expanding amount of R&D spending in developing semiconductors by non-semiconductor companies.

Second, massive investment is moving into industries where data is being sourced, processed and analyzed, either at the edge or at the core of different networks. The workloads in these industries are changing to process data and gain insights about customers and how they use products. These areas are driving the economics of business, and they will be the biggest beneficiaries. For instance, hyperscalers (also known as the ‘whales’) are already showing to be the strongest players in this space, and they will continue to grow.

Finally, the semiconductor market will expand and accelerate in the second half of the year as the worldwide vaccination against COVID is proven. Most analysts and economists anticipate a synchronized economic recovery. That means multiple regions of the world grow in synchronism – as opposed to a situation where some parts of the world, markets are growing and in other parts of the world, markets are not growing. When a synchronized economic recovery happens, semiconductor growth increases dramatically in terms of growth rate, primarily because GDP is also growing significantly.

You said drivers for this growth is data processing and analytics. To be specific, which vertical markets will be the largest contributors?

Among the highest growth verticals today, the 5G market is on a rapid ramp. Companies such as Qualcomm and MediaTek report growing revenues driven by their 5G semiconductors that fuel many different industries. The 5G market is really about enabling new networks for so many industries beyond consumer voice and video – including factories, gaming, healthcare, and transportation.

The second vertical is the Industrial IoT market. It is the fastest growing portion of semiconductors. Industrial IoT refers to the use of semiconductors in manufacturing settings where chips are embedded sensors, controllers, and computers in the manufacture of products. These are chips in industrial PCs or Programmable Line Controllers (PLCs). Factory automation is driving the digital transformation that is creating a sizable opportunity for semiconductors where there are many legacy or brownfield systems as well as many new greenfield systems.

New systems are created to dramatically improve manufacturing efficiency and lower manufacturing costs to design products much more efficiently. These range from systems for food and beverage packaging all the way to next-generation planes and aircrafts, such as electric personal aircrafts, and everything in between. Manufacturing systems are a big area for growth in the coming decade. Siemens, as a leader in industrial automation is at the forefront enabling the digital transformation of these industries.

The third vertical is the data center world that includes companies in the business of processing loads of data. For example, social media companies such as Facebook, Instagram or Google or digital shopping companies are providing services with search engines, and supporting connectivity between people to create social networks and ecosystems around social networks driven by search and commerce. The demand is rapidly growing because of the increasing adoption of visual and audio-based communication interfaces that create unique experiences. The need for computing in the data center world is dramatically growing and changing, driving the requirement for more and more powerful semiconductors. The critical issue here is that the sheer volume of data and the amount of computing power is so large that efficiency becomes paramount to decide how much data center to build. More and more companies in this business such as Google, Microsoft and Amazon are building their own chips to get much higher computational efficiency with new and diverse workloads with a much more efficient power footprint. If you look at the R&D spending of these companies and what is driving the demand for more R&D, it really comes down to high-performance power-efficient workload processing the data in the data center.

The last market is transportation. People may refer to automotive, but I prefer to call it transportation. It encompasses automotive, robotics, and autonomous vehicles and pulls in safety and security. It captures driver assistance, safety systems in cars, systems in drones, systems and robots that provide a transportation mechanism in an environment that is more autonomous, more electrical and more driven by safety constraints.

Through all of this, has COVID played a role?

COVID triggered remote working that boosted sales of data centers, networking gear, memory, as well as laptops and tablets needed for the home office. Specific technology sectors and specific semiconductor categories have been growing very well.

On the other hand, because of COVID’s impact on the supply chain together with other things affecting the automotive industry, the automotive industry had one of its worst performing years. It’s recovering now, but COVID made it clear that not all the technology sectors are equal. Some enjoy stronger growth because of what was in the environment due to COVID.

Some normalization is under way now, but spending on traditional consumer products and consumer durables held back until we got into the holiday period, when sales dramatically took off. For the better part of the year, GDP suffered a significant drop because of the drop in spending. In the U.S., consumer spending corresponds to about 65% of the GDP, so a big part of GDP drop had to do with falling services and consumer spending. COVID had an impact on some industries. According to some people, COVID accelerated digital everything.

In light of this anticipated explosive growth, how will EDA and Siemens EDA change?

For most of its history, EDA has been tied to R&D spending of semiconductor companies. In the future, EDA will not be limited to the R&D budgets of only semiconductor companies. Rather, it will be driven by R&D spending from non-semiconductor companies. We talked about automotive and hyperscalers, but we also have semiconductors in several other industries. And more systems companies build products that include semiconductors. All these activities expand the EDA market.

It is critical for EDA to adopt a system perspective and integrate the notion of a product life cycle in the management of electronic products. A system perspective expands the focus beyond semiconductors to include the board, package, modules they’re installed on, the systems they’re built in, the environment the system is operating in.

EDA needs to deliver all of the above. For example, automotive manufacturers need to know how a particular device is behaving in a car traveling in various types of traffic and environmental conditions. Today, this problem is addressed by collecting tons of data from real-world data or synthesized scenarios. The system scenarios need to be presented into environments modeling the operation of the chip and the software running on the chip. Bringing together the system perspective and encapsulating chip, software, sensor, system and environment is imperative.

Validation and certification of systems is crucial. This is carried out by creating a virtual environment to exercise and demonstrate the scenarios where these chips operate in, the software it needs to operate in, to validate and certify the chip together with the software operating in these environments to a given level of confidence.

Safety and security are as important as the basic functionality of the product. It is increasingly difficult to decouple them, making virtual certification a mandatory approach and drives the notion of digital twin, the underlying theme of a system perspective.

This perspective is not unique to Siemens. Siemens was certainly a pioneer in driving the vision around the digital twin. Today, we have digital twins for cars, jet engines, aircrafts, as well as for the human body in different pieces. Rather soon, we will have digital twins for biological systems, electrical systems, and mechanical systems.

The next frontier for EDA is where the system perspective and digital twin come into play. Ultimately, EDA has to deal with heterogeneous multi-die systems that will result from advancements in semiconductor and packaging technologies and progress in larger capacity and higher performance.

I believe the digital twin world, the IC world and the product management world are going to come together to define the future of EDA.

In terms of EDA market growth prospects, the biggest opportunities come from verification, from chips to systems, to software. Among them, verification and validation of systems is the fastest growing part of EDA today, making it the priority for investment. It is fundamental to offer software-based solutions, both dynamic simulation/analysis and static technologies, as well as hardware-based verification platforms, across emulation and prototyping. For instance, we’re seeing a big renaissance in formal verification and more systematic coverage technologies and analysis techniques leveraging AI and ML.

In hardware-assisted verification platforms, the main drivers are the expanding sizes of chips, not just single-die but multi-die solutions. Another driver is the need to perform software workload-based analysis, not just analysis of the functionality of the chips, but the workloads we’re running on them and what does that mean in terms of performance and power consumption.

Several issues can translate in big R&D opportunities, such as, does the software run in different scenarios? Can you create scenarios that are attacking the chip, and does the software behave differently? Can you use learning techniques to understand how the chip should properly behave in a normal situation? What about hardware and software? And how should they change in situations where there’s been some type of compromise of safety or security?

The biggest questions in security and safety are how much is enough, forcing a re-definition of coverage to become more systematic and include statistical techniques driving a renaissance in the definition and design of experiments.

In all these areas, AI is an enabling technology. AI can be applied across all because there’s a lot of data to work with. I believe that the application of more and more advanced concepts taken from statistics and stochastics together with artificial intelligence are going to drive the next wave of innovation in EDA.

To conclude, do you anticipate a wave of industry consolidation or industry proliferation of new companies, like spin-offs and startups?

Right now, company valuations in the semiconductor industry are sky high because of strong growth and a loose monetary policy. Companies have acquisition currencies they didn’t have a decade ago, and they’re able to take advantage of it. If you look at the total dollar value of M&A in 2020, it’s the highest ever in the semiconductor industry. There’s an increasing recognition that semiconductors are capturing profits, and, as long as we have these asset prices, I expect there’s going to be more consolidation.

This can be seen from the three big announcements of last year: Nvidia-Arm, AMD-Xilinx, and Marvell-Inphi. We can expect to see more consolidation as companies review their product portfolio vis-à-vis the markets they want to grow in and build a leading position in.

A large number of companies started over the past five years during the hype of the Gartner technology cycle, developed AI chips and semiconductors for AI and ML. Right now, M&A books of investment banks are growing significantly not only driven by semiconductors, but also by non-semiconductor/system companies buying semiconductor companies. Apple, Google, Microsoft, Amazon have been doing that. We can expect it to continue.

Some companies that started years ago will no longer get funded, while others will continue to get funded. There’s one fundamental difference between these two classes of companies. Companies in the first category designed a chip but they don’t have a workload to evaluate and benchmark the chip for a specific industry. They have been generic in their approach. Companies in the second category focused on a specific industry, a specific market, and have a specific set of workloads. These companies are the ones who get evaluated and can immediately demonstrate their value for the workload.

Today, there is a flight-to-quality. That is, the money is following the quality of companies that demonstrated the ability to design new computer architectures, a software architecture, and perform workload analysis to deliver unique value for that workload.

While many of the companies in that first category are not around anymore, those who have been the flight-to-quality recipients are going to continue to thrive.

_________________________________________________________

About Ravi Subramanian

About Ravi Subramanian

Ravi Subramanian is a Senior Vice President responsible for all IC Verification Solutions at Siemens EDA. The division’s business spans Analog, RF and mixed-signal circuit simulation and analysis products, digital IC software/hardware verification and validation products and solutions, serving automotive, wireless, data center and IoT markets.